As 2019 draws to a close, only the most unflinchingly loyal industry players are refusing to accept that the condominium market is correcting. Listed developers are blaming LTV restrictions imposed by the Central Bank in early 2019. This has not helped, but blaming this alone, is like closing the stable door, in this case, years after the horse has already bolted. The reasons for correction are clear:

• A 20-year bull run, where Bangkok condo prices have multiplied by 700%

• Prime land price inflation at twice the rate of condo price inflation, whereby it has no longer been able to develop condos profitably for the past 3-4 years

• A loss of confidence in the Thai domestic market

• Thai household debt off the charts to hitherto unseen heights

• A 20-year bull run, where Bangkok condo prices have multiplied by 700%

• Prime land price inflation at twice the rate of condo price inflation, whereby it has no longer been able to develop condos profitably for the past 3-4 years

• A loss of confidence in the Thai domestic market

• Thai household debt off the charts to hitherto unseen heights

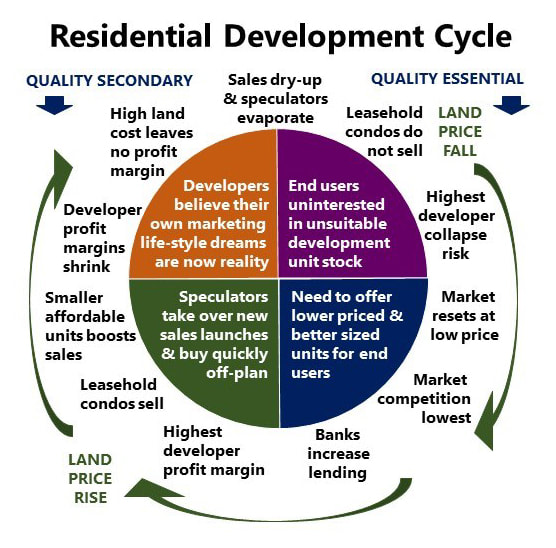

We are now at the very top of the residential development cycle. All the ingredients are in place for the perfect storm. Most developers are still in denial, as admitting to decline, imperils a damaging self-fulfilling prophecy. Those with the biggest debts and overpriced land are most at risk. It just remains to be seen how bad it will be, and how far will they fall?

The Curse of the Listed Developer

The concept of listed developers increasing profits and earnings every year, hits a roadblock when the property market corrects. Real estate by nature is more cyclical than other industries and is only a safe investment haven when the market is rising.

However, because of listed status demands, developers need to continue buying land, even when overpriced, in order to continue showing growth. They have to buy land on the assumption that property prices will continuing rising. This inevitably stops, and, they end up caught with an inventory of overpriced, unprofitable properties, that are out of tune with the market in recession.

Developers with strongest balance sheets, can fire-sell units quickly once the market turns, and slash prices before the race to the bottom starts in earnest. Those that cannot, because they paid too much for the land, risk a huge potential distressed debt problem, and some will ultimately find themselves having leapt off the listed market cliff, lemming style.

The Curse of the Listed Developer

The concept of listed developers increasing profits and earnings every year, hits a roadblock when the property market corrects. Real estate by nature is more cyclical than other industries and is only a safe investment haven when the market is rising.

However, because of listed status demands, developers need to continue buying land, even when overpriced, in order to continue showing growth. They have to buy land on the assumption that property prices will continuing rising. This inevitably stops, and, they end up caught with an inventory of overpriced, unprofitable properties, that are out of tune with the market in recession.

Developers with strongest balance sheets, can fire-sell units quickly once the market turns, and slash prices before the race to the bottom starts in earnest. Those that cannot, because they paid too much for the land, risk a huge potential distressed debt problem, and some will ultimately find themselves having leapt off the listed market cliff, lemming style.

|  |

A new report by CAS Capital (Thailand), an independent real estate asset management and construction specialist, paints a gloomy but realistic picture of the local condominium scene

Incentivization or Desperation?

Five years ago, a new condo launch was only considered successful, if 90%+ of the units were sold at launch. In 2019, a developer considers a 40% launch sales rate a great success, to be broadcast loudly!

For the past decade, most condo buyers were speculators or investors. Properties were bought at launch, and flipped to other buyers during construction, which could last three or four years.

As long as prices continued to rise, things worked very well. What we are seeing now, is developers dropping prices below launch levels, which leaves the remaining early speculators, left high and dry. Under these circumstances, it is obvious why speculators are evaporating and condo sales in Q4 2019 are the worst in a decade.

Thai buyers are key to condo market sales, given the legal requirement to maintain minimum local ownership. Unprecedented domestic household debt levels therefore further exacerbates market frailty. The Central Bank, alarmed by rising debt defaults, is trying to reign in lending, but in spite of this, the bank NPL ratio has still surged upwards in Q4 2019. Furniture and fit-out packages are now standard for condo marketing.

Many developers have gone further by offering additional incentives. The Pattaya market has particularly seen the introduction of investment schemes that offer guaranteed returns of up to 10% per annum, for up to 10 years for an asset class with a market yield of 3-4%. Some more extreme schemes also guarantee to buy the condo back for between 105% and 150% of purchase price!

This has led to a bizarre situation, where only investment schemes are selling, as buyers have lost faith in property. Slick marketing camouflages substance, and both local and foreign buyers have been enticed. What buyers do not appreciate is that they may be paying double the market price for their condo. They are also 100% reliant upon the developer, most of whom lack capital, completing the project, and supporting the investment to maturity. If the developer fails, they will end up with a condominium worth half what they paid for, and no income, assuming the project gets finished!

A number of specialist brokerages market investment schemes like this. In October 2019, the first of these collapsed, which may be the beginning of a series of failures, where a host of gullible consumers end up losing all they have invested.

Five years ago, a new condo launch was only considered successful, if 90%+ of the units were sold at launch. In 2019, a developer considers a 40% launch sales rate a great success, to be broadcast loudly!

For the past decade, most condo buyers were speculators or investors. Properties were bought at launch, and flipped to other buyers during construction, which could last three or four years.

As long as prices continued to rise, things worked very well. What we are seeing now, is developers dropping prices below launch levels, which leaves the remaining early speculators, left high and dry. Under these circumstances, it is obvious why speculators are evaporating and condo sales in Q4 2019 are the worst in a decade.

Thai buyers are key to condo market sales, given the legal requirement to maintain minimum local ownership. Unprecedented domestic household debt levels therefore further exacerbates market frailty. The Central Bank, alarmed by rising debt defaults, is trying to reign in lending, but in spite of this, the bank NPL ratio has still surged upwards in Q4 2019. Furniture and fit-out packages are now standard for condo marketing.

Many developers have gone further by offering additional incentives. The Pattaya market has particularly seen the introduction of investment schemes that offer guaranteed returns of up to 10% per annum, for up to 10 years for an asset class with a market yield of 3-4%. Some more extreme schemes also guarantee to buy the condo back for between 105% and 150% of purchase price!

This has led to a bizarre situation, where only investment schemes are selling, as buyers have lost faith in property. Slick marketing camouflages substance, and both local and foreign buyers have been enticed. What buyers do not appreciate is that they may be paying double the market price for their condo. They are also 100% reliant upon the developer, most of whom lack capital, completing the project, and supporting the investment to maturity. If the developer fails, they will end up with a condominium worth half what they paid for, and no income, assuming the project gets finished!

A number of specialist brokerages market investment schemes like this. In October 2019, the first of these collapsed, which may be the beginning of a series of failures, where a host of gullible consumers end up losing all they have invested.

A fundamental indicator of the health of the local economy

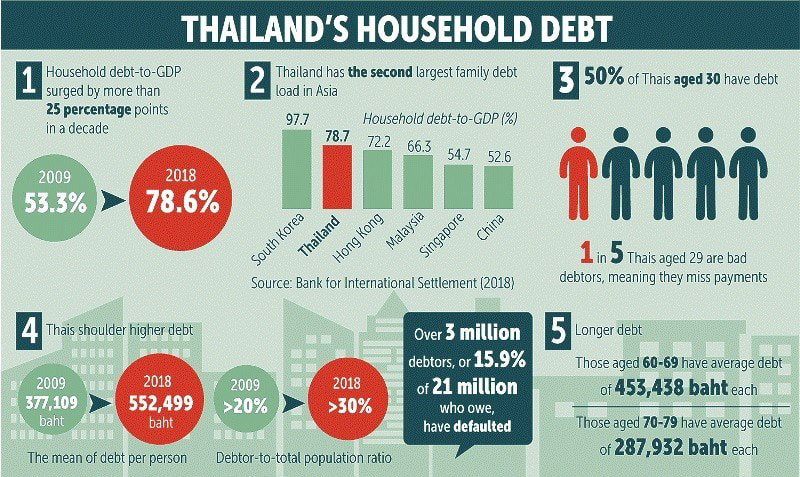

1. Household debt-to-GDP surged by more than 25 percentage points in a decade, from 53.3% in 2009 to 78.6% in 2018.

2. Thailand has the second largest family debt load in Asia (78.7), after South Korea (97.7). Others: Hong Kong (72.2), Malaysia (66.3), Singapore (54.7) and China (52.6).

3. 3.50% of Thais aged 30 have debt. One in five Thais aged 29 are bad debtors, meaning they miss payments.

4. Thais shoulder higher debt. From 377,109 baht in 2009 to 552,499 baht in 2018 (based on the mean debt per person). Debtor to total population ratio

has increased from 20% in 2009 to 30% in 2018. Over three million debtors, or 15.9% of 21` million who owe, have defaulted.

5. 5. Longer debt. Those aged 60-69 have average debt of 453,438 baht each. Those aged 70-79 have average debt of 287,932 baht each.

2. Thailand has the second largest family debt load in Asia (78.7), after South Korea (97.7). Others: Hong Kong (72.2), Malaysia (66.3), Singapore (54.7) and China (52.6).

3. 3.50% of Thais aged 30 have debt. One in five Thais aged 29 are bad debtors, meaning they miss payments.

4. Thais shoulder higher debt. From 377,109 baht in 2009 to 552,499 baht in 2018 (based on the mean debt per person). Debtor to total population ratio

has increased from 20% in 2009 to 30% in 2018. Over three million debtors, or 15.9% of 21` million who owe, have defaulted.

5. 5. Longer debt. Those aged 60-69 have average debt of 453,438 baht each. Those aged 70-79 have average debt of 287,932 baht each.

RSS Feed

RSS Feed